Global share markets mostly rose again over the last week helped in particular by good US news on inflation adding to confidence that interest rates have peaked. For the week US shares rose 2.2%, Eurozone shares gained 3.3% and Japanese shares rose 3.1%. Chinese shares fell 0.5% with ongoing concerns about the Chinese property market. The continuing global rebound also helped push up Australian shares which rose 1% led by IT, property, material and health stocks. 10-year bond yields fell by 15-20 basis points on optimism major central banks have finished raising rates. Oil prices fell with rising inventories. Metal and iron ore prices and the $A rose as the $US fell.

More good news. The past week has seen more good news that has helped push shares higher and bond yields lower: inflation has continued to surprise on the downside – this time from the US and UK – supporting the view that rates have peaked; US economic data has been consistent with a soft landing; US profit results continue to surprise on the upside making it the best reporting season in two years; policy uncertainty diminished a bit with the US and China looking to ease tensions and the US Congress averting a shutdown with temporary funding; the war in Israel has not widened to include major oil producers and oil prices are well below their level of prior to Hamas’ attacks; and in Australia wages and jobs data came in marginally stronger but roughly in line with RBA forecasts suggesting for now at least that a rate hike in December is unlikely. All of this is combining with a positive seasonal pattern that sees strength from around now until around May in the US (or July in Australia). And so far, the breadth of the rally in shares has been broad based which is positive from a technical perspective.

Source: Bloomberg, AMP

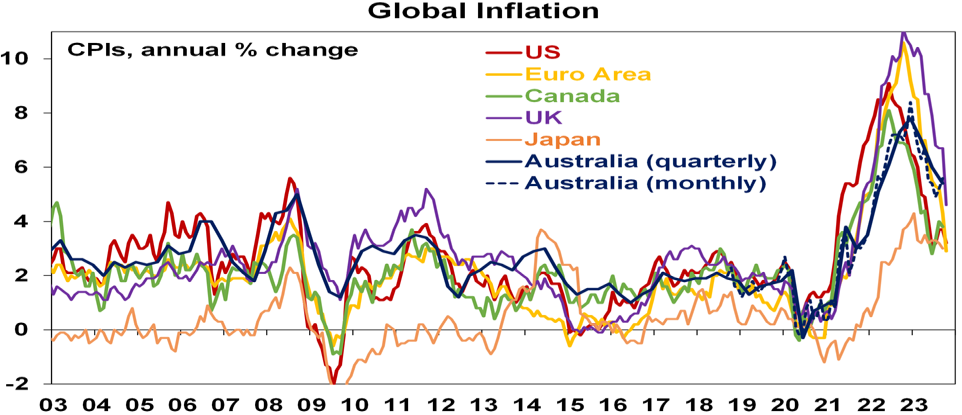

The good news on inflation is evident in the next chart showing inflation rates in major developed countries. While there is high anxiety about sticky services inflation, inflation is continuing to fall about as quickly as it went up. Relative to the US, Canada, Europe and the UK, Australian inflation lagged on the way up and peaked a little later (partly reflecting the slower reopening from covid) and it’s doing the same on the way down so there is no reason to be alarmed that its higher than in North America and Europe. More broadly, because the surge in global inflation led that in Australia, the decline in global inflation points to a further decline in Australian inflation ahead.

Source: Bloomberg, AMP

Of course there are still some significant risks to keep an eye on: the risk of a flare up in the war in Israel to involve Iran is high; the risk of recession remains high; uncertainty remains high around China’s property sector; high bond yields still threaten share markets; sticky services inflation is likely to keep central banks hawkish for a while with a “high for longer” message on rates; the risk of another rate hike in Australia is still high; its hard to see a sustained easing in US/China tensions; US Government shutdown risks will return next year as funding was only extended to January 19 and February 2 depending on the department and the US budget deficit is not on a sustainable path; and investor sentiment is yet to fall to levels associated with major market bottoms (not that it always has too). So, shares are still likely to remain volatile.

The Beatles’ last three songs. Since 1995 The Beatles have released three new songs built on rough recordings made on cassette by John Lennon in the 1970s. On first hearing the just released Now and Then it sounded the weaker of the three but after a few listens I have concluded its far superior. Listening to it does bring on a bit of emotion for many Beatles’ fans – not just because it could really turn out to be the last Beatles’ song but because it works as an expression of the love between John and Paul, but also because of Paul’s homage to George with the slide guitar section, the amazing Beatlesque strings, Ringo’s drumming and the addition of Paul and Ringo’s vocals. The Peter Jackson directed video is a real treat. But Free as a Bird and Real Love are also worth checking out.

Economic activity trackers

Our Economic Activity Trackers are still not showing anything decisive for the direction of economic activity.

Levels are not really comparable across countries. Based on weekly data for eg job ads, restaurant bookings, confidence and credit & debit card transactions. Source: AMP

Major global economic events and implications

US economic data was softish adding to hopes for a soft landing. October retail sales slowed but this followed several strong months so it’s a bit hard to read too much into one slower reading.

Source: Macrobond, AMP

US manufacturing conditions improved in the New York and Philadelphia regions but still remain softish and small business optimism and industrial production fell. Home building conditions weakened further in November pointing to further housing sector weakness ahead despite a rise in starts in October and jobless claims are continuing to edge higher.

Source: Macrobond, AMP

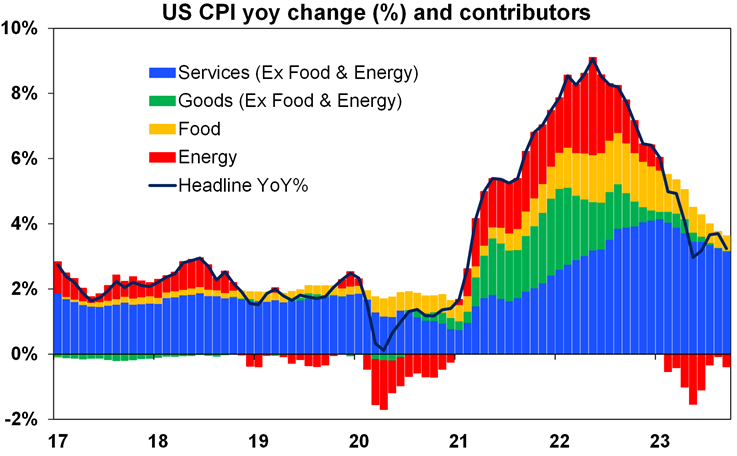

US inflation surprised on the downside in October adding to the case that the Fed has finished hiking, although sticky services inflation (blue bars in the next chart) will likely see the Fed retain a tightening bias and a “high for longer” message for now. CPI inflation was flat in the month and fell to 3.2%yoy (down from a high of 9.1% mid last year), core CPI inflation fell to 4%yoy and producer price inflation slowed to 1.3%yoy.

Source: Bloomberg, AMP

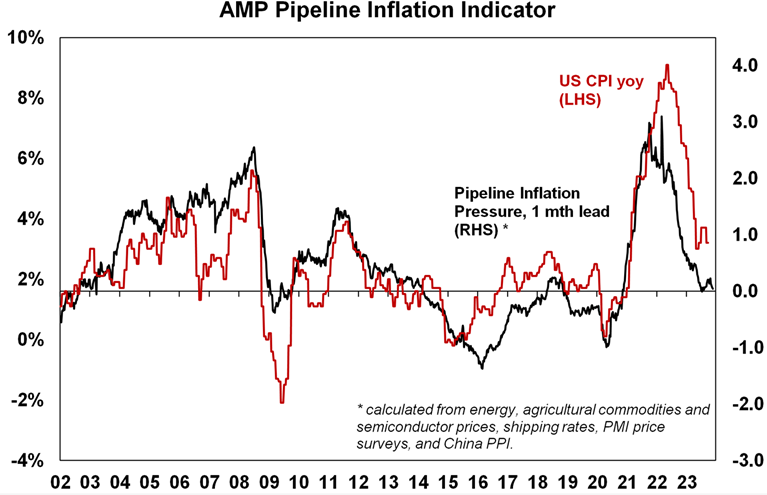

As Fed Chair Powell has said the fall in inflation will “come in lumps and be bumpy”, but our US Pipeline Inflation Leading Indicator continues to point down.

Source: Bloomberg, AMP

The US September quarter earnings reporting season is now largely wrapped with beats running at the highest in two years. 94% of S&P 500 companies have now reported with 82.1% beating expectations, well above the norm of 76% and the strongest in 2 years. Earnings growth for the quarter has improved to +4%yoy from +0.6% at the start of the reporting season.

UK inflation also fell more than expected in October with stagnant September quarter GDP, although wages growth remains strong. Expect the Bank of England to remain on hold but retain a tightening bias for now. The CPI was flat in the month and fell to 4.6%yoy and is down from a high of 11.1%yoy in October last year and core inflation fell to 5.7%yoy from 6.1%. Producer price inflation slowed to just 0.6%yoy. Wages growth slowed but remained strong at 7.7%yoy and well above most other developed countries including Australia (see below under Australia).

Japanese September quarter GDP contracted a greater than expected 0.5%qoq. This was down from 1.1%qoq growth in the June quarter and reflected flat consumer spending, falls in business and housing investment and detractions from trade and inventories. Producer price inflation slowed to 0.8%yoy from 2.2%yoy and is down from a high of over 10%yoy in 2022. Both are likely to leave the BoJ cautious in tightening monetary policy further.

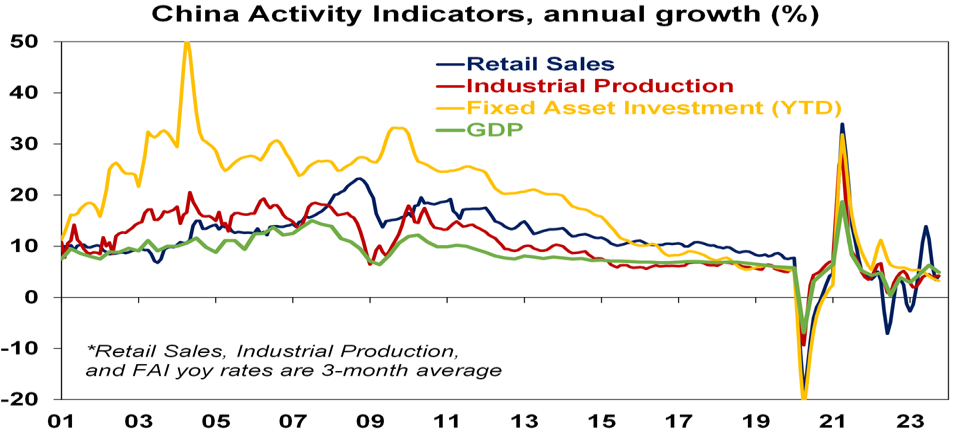

Chinese economic activity indicators for October showed more signs that growth has bottomed. Retail sales came in stronger than expected at 7.6%yoy and industrial production and investment were roughly in line with expectations. Growth looks on track for around 5% this year, but the key risk remains the property sector where sales, prices and investment remain weak. The latter probably explains recent reports that the PBOC will provide 1 trillion Renminbi (about $A215bn) in cheap housing finance.

Source: Bloomberg, AMP

Australian economic events and implications

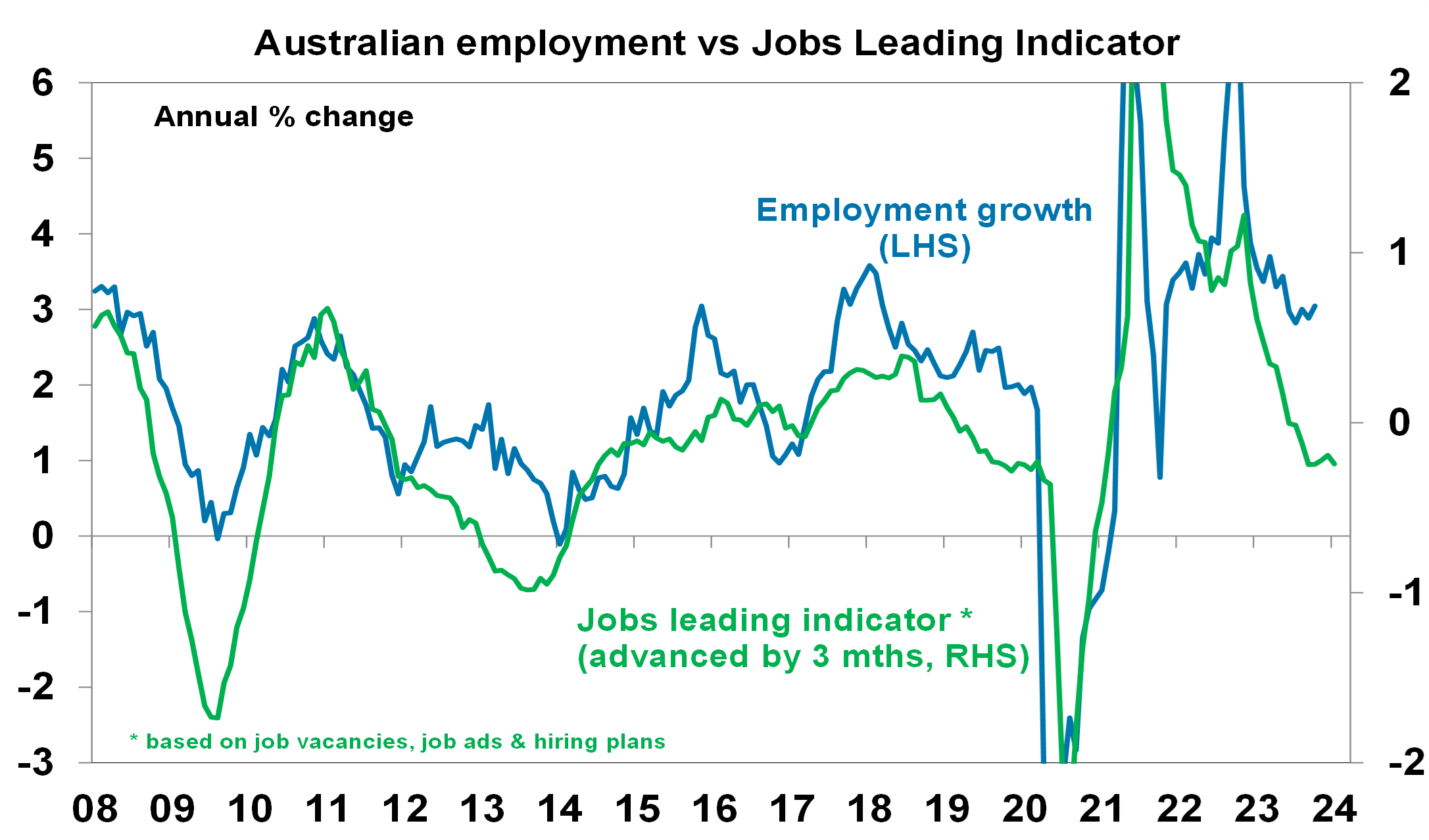

Australian jobs data surprised on the upside in October, but unemployment is roughly tracking RBA forecasts and jobs leading indicators continue to point to softness ahead. The 55,000 gain in employment was likely boosted by referendum workers and was mainly in part-time jobs so some reversal is likely this month. The jobs market is still tight but its gradually easing with unemployment (at 3.7%) and underemployment (at 6.3%) both up from their lows in October last year and various leading indicators point to softer jobs growth head including a rising trend in applicants per Seek ad a rise in consumer unemployment expectations. Our Jobs Leading Indicator continues to point to softer jobs growth.

Source: ABS, AMP

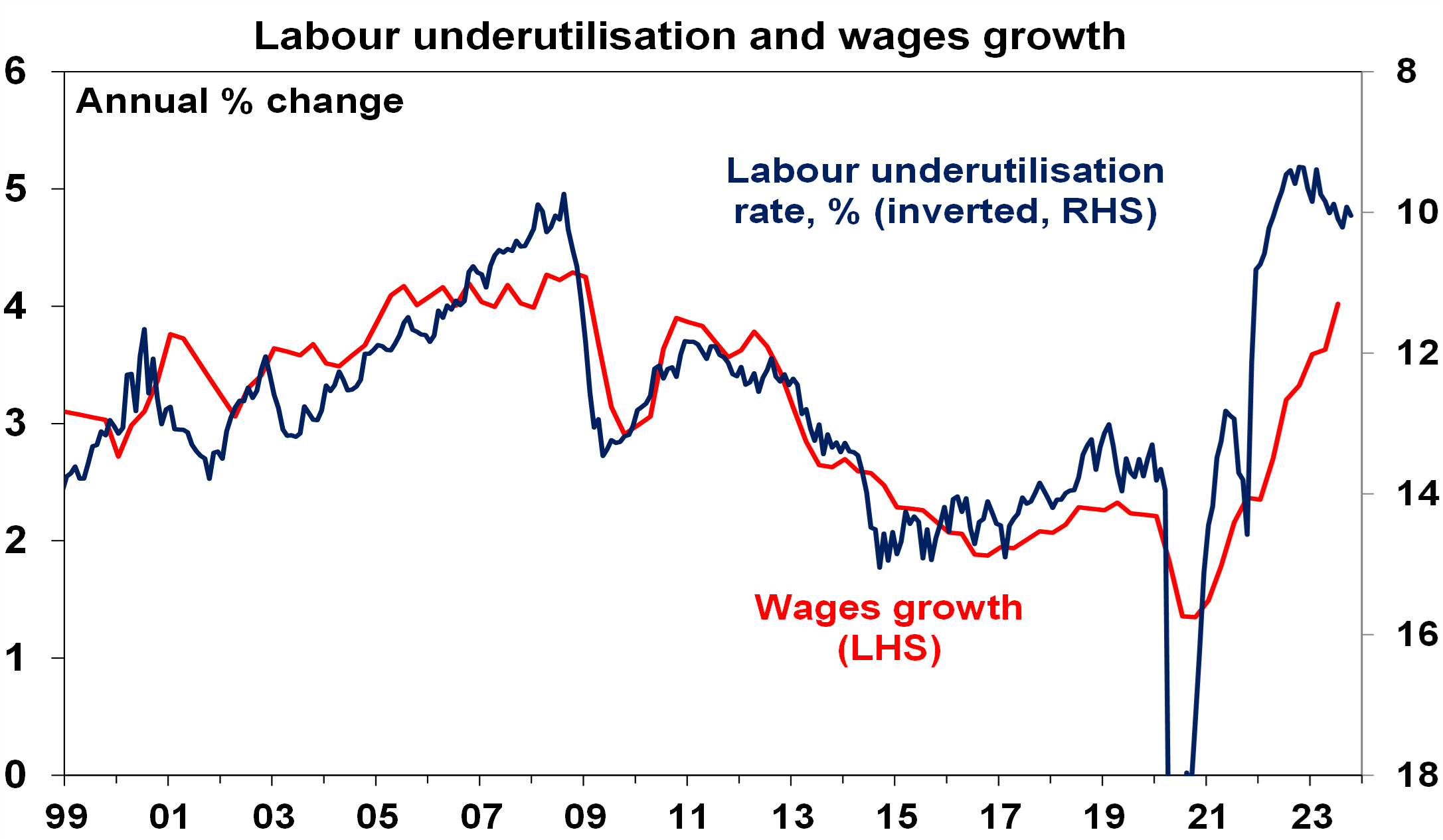

Wages growth rose to 4%yoy in the September quarter, with this year’s faster rise in minimum and award wages adding 0.3 percentage points to wages growth. There are three key points.

- First, the acceleration has been broad based across industries.

- Second, signs of an easing in the labour market point to a peaking in wages growth next year.

Source: ABS, AMP

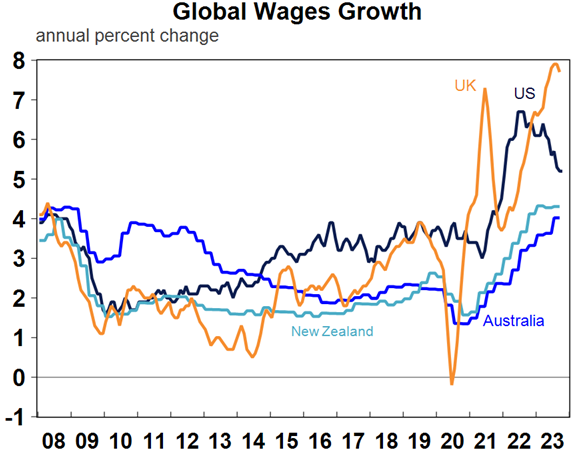

- Finally, despite the acceleration, Australian wages growth remains modest relative to other countries.

Source: ABS, AMP

Both the wages and jobs data were a bit stronger than the RBA forecast but its marginal and not enough on their own to bring on another rate hike. The 3.7% unemployment rate for October is roughly consistent with the RBA’s forecast for 3.8% this quarter and the RBA forecast a rise in wages growth to 4% and with its business liaison program pointing to a slowing in wages growth next year it’s not likely to be too concerned. So, on their own they are unlikely to trigger a rate hike next month. Our base case remains that rates have peaked, but the risk of another hike remains high (at around 40%) particularly if upcoming retail sales and inflation data are stronger than expected and if productivity growth remains weak.

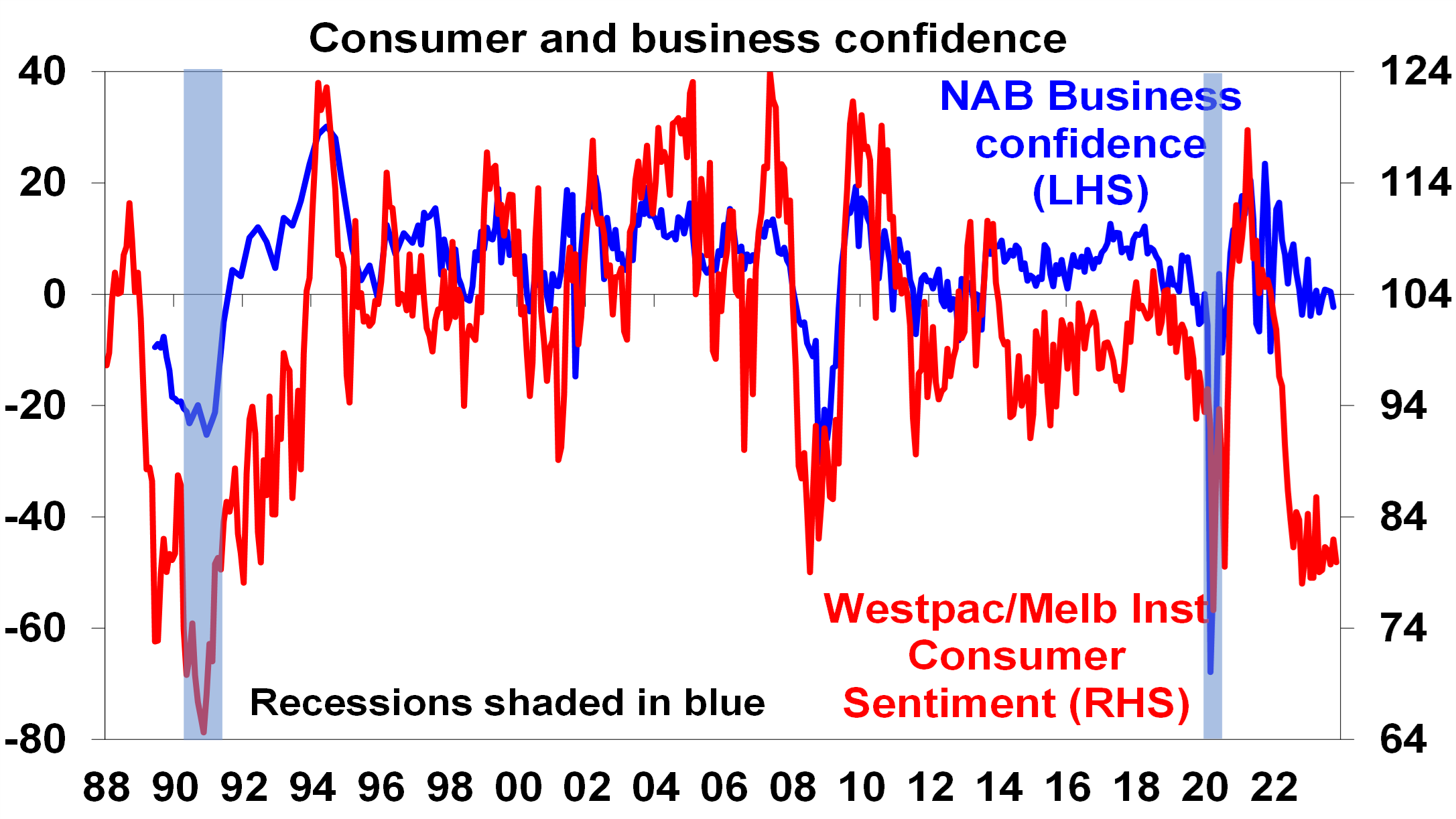

Australian consumers still depressed, but business conditions still okay. The November Westpac/MI consumer survey showed consumer confidence wallowing at recessionary levels and nearly 40% planning to spend less on gifts this Christmas. By contrast business confidence remains far more resilient and business conditions are above average.

Source: Westpac/MI, NAB, AMP

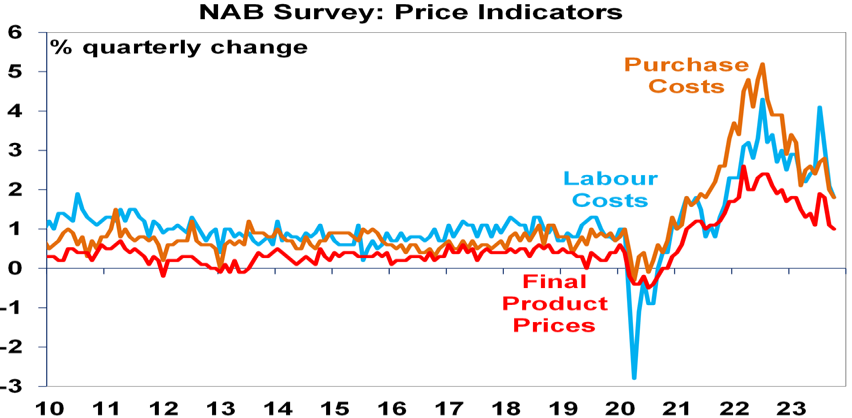

But the good news is that the NAB survey showed a further fall in cost and price pressures after a mid-year spike. This adds to confidence that the rise in minimum and award wages has not led to an ongoing surge in other wages.

Source: NAB, AMP

In other economic data, HIA data showed that new home sales remained low in October consistent with high interest rates and consumers continuing to regard now as a poor time to buy property.

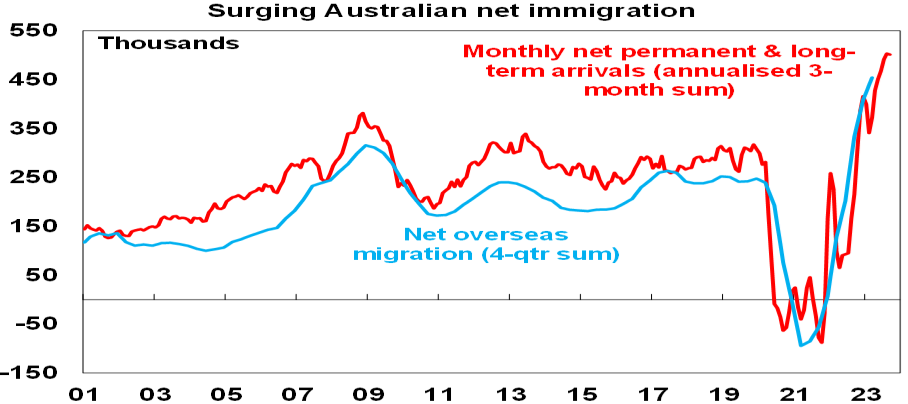

Meanwhile monthly permanent and long term arrivals data point to a continuing surge in population growth with net migration running around 500,000 people or more per annum. This is way above last year’s March budget forecast of 180,000 for 2022-23 and it’s hard to see it falling back to the 315,000 forecast for this financial year in this year’s May budget. With home building depressed the housing shortfall will worsen this financial year with Australia on track to build around 70,000 less dwellings than we need adding to an existing shortfall of around 120,000 dwellings.

Source: ABS, AMP

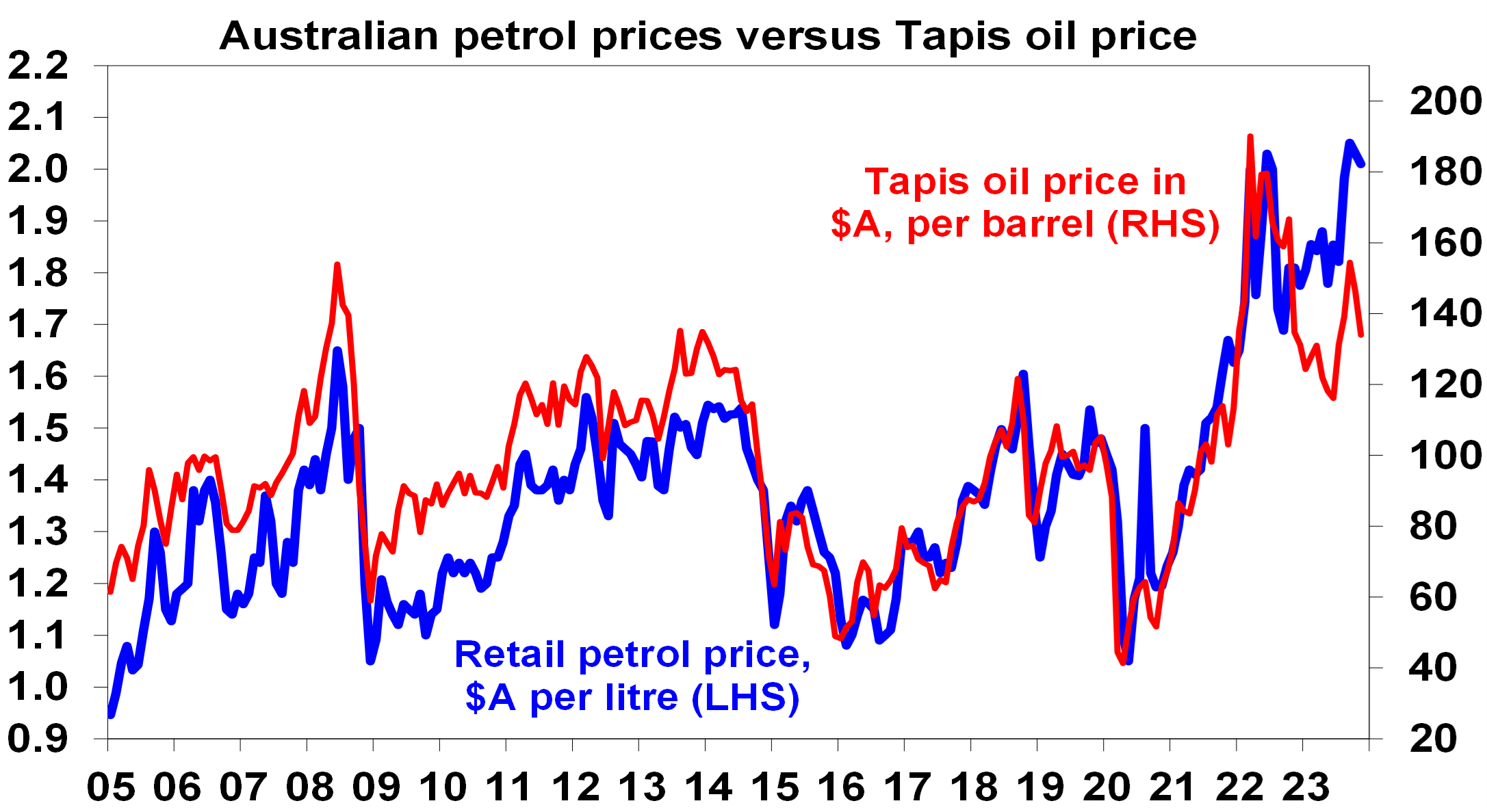

The DP World ports and Optus disruptions in the past two weeks highlight the economy’s vulnerability to what amounts to supply side shocks. Fortunately, both look to have been relatively brief although there is more risk around DP World given strike action, but extended supply shocks would risk adding to inflation pressures. The good news is that the war in Israel has not so far led to global oil supply disruptions and global oil prices are around $US7/barrel lower than just before the Hamas attacks, so based on current oil prices Australian petrol prices should be heading well below $2/litre.

Source: Bloomberg, MotorMouth, AMP

In some other good news, the Federal budget for the first 3 months of the financial year is running around $6bn better than projected in the May budget. If it continues the projected $14bn deficit for this financial year could turn out to be a modest surplus.

What to watch over the next week?

In the US, the minutes from the Fed’s last meeting (Tuesday) are likely to emphasise that it will proceed “carefully” but stands ready to hike again if needed and will keep rates high for longer. On the data front, leading indicators for October (Monday) are likely to have fallen further, existing home sales (Tuesday) are likely to remain weak, durable goods orders (Wednesday) are likely to fall back after a strong rise in September and business conditions PMIs for November (Friday) are also likely to fall slightly.

Canadian inflation (Tuesday) is expected to fall to 3.3%yoy.

Eurozone business conditions PMIs (Thursday) are likely to remain weak.

Japanese CPI inflation (Friday) is likely to rise to 3.4%yoy, with core inflation likely to rise slightly to 2.7%yoy. Business conditions PMIs (also Friday) are likely to weaken a bit further.

In Australia the focus will be on monetary policy with the minutes from the last RBA meeting (Tuesday) likely to provide some indication as to how close the decision to raise rates again was and along with Governor Bullock’s participation on a panel (Tuesday) and a speech (Wednesday) are all likely to be watched for guidance as to how strong the RBA’s softened tightening bias is. Business conditions PMIs (Thursday) are likely to remain soft.

Outlook for investment markets

The next 12 months are likely to see a further easing in inflation pressure and central banks moving to get off the brakes. This should make for reasonable share market returns, provided any recession is mild. But for the near-term shares are at high risk of a further correction given high recession and earnings risks, the risk of high for longer rates from central banks, high bond yields which threaten share market valuations and the risk that the war in Israel escalates to include significant oil producing countries like Iran.

Bonds are likely to provide returns above running yields, as growth and inflation slow and central banks become dovish.

Unlisted commercial property and infrastructure are expected to see soft returns, reflecting the lagged impact of the rise in bond yields on valuations. Commercial property returns are likely to remain negative as “work from home” continues to hit space demand as leases expire.

With an increasing supply shortfall, our base case remains that home prices have bottomed with more gains likely next year, albeit at a slower pace. However, uncertainty around this is high given the lagged impact of interest rate hikes and the likelihood of higher unemployment both of which could push prices down again.

Cash and bank deposits are expected to provide returns of around 4-5%, reflecting the back up in interest rates.

The $A is at risk of more downside in the short term on the back of relatively lower short term interest rates in Australia and global uncertainties, but a rising trend is likely over the next 12 months, reflecting a downtrend in the overvalued $US and the Fed moving to cut interest rates.

What you need to know

While every care has been taken in the preparation of this article, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent AMP. This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.

The information on this page was current on the date the page was published. For up-to-date information, we refer you to the relevant product disclosure statement, target market determination and product updates available at amp.com.au.