Key points

– Since its February 2021 high of nearly $US0.80 the $A has fallen on the back of worries about the global growth outlook, worries about China, the strong $US and relatively less aggressive monetary tightening by the RBA.

– However, there is good reason to expect the $A to rise into next year: it’s undervalued; short term interest rate differentials look likely to shift in favour of Australia; sentiment towards the $A is negative; commodities still look to have entered a new super cycle; and Australia has a solid current account surplus.

– There is a case for Australian-based investors to tilt a bit to hedged global investments but while maintaining a still decent exposure to foreign currency.

– The main downside risk for the $A would be if there is a hard landing globally and/or in Australia next year.

Introduction

Changes in the value of the Australian dollar are important for Australian investors as they directly impact the value of international investments and indirectly effect the performance of domestic assets like shares via the impact on Australia’s global competitiveness. They also impact the cost of travelling overseas and import prices. But currency movements are also very hard to get right. Over the last few years, the $A has been soft. This note takes a look at the outlook for the $A.

Why has the $A been so soft?

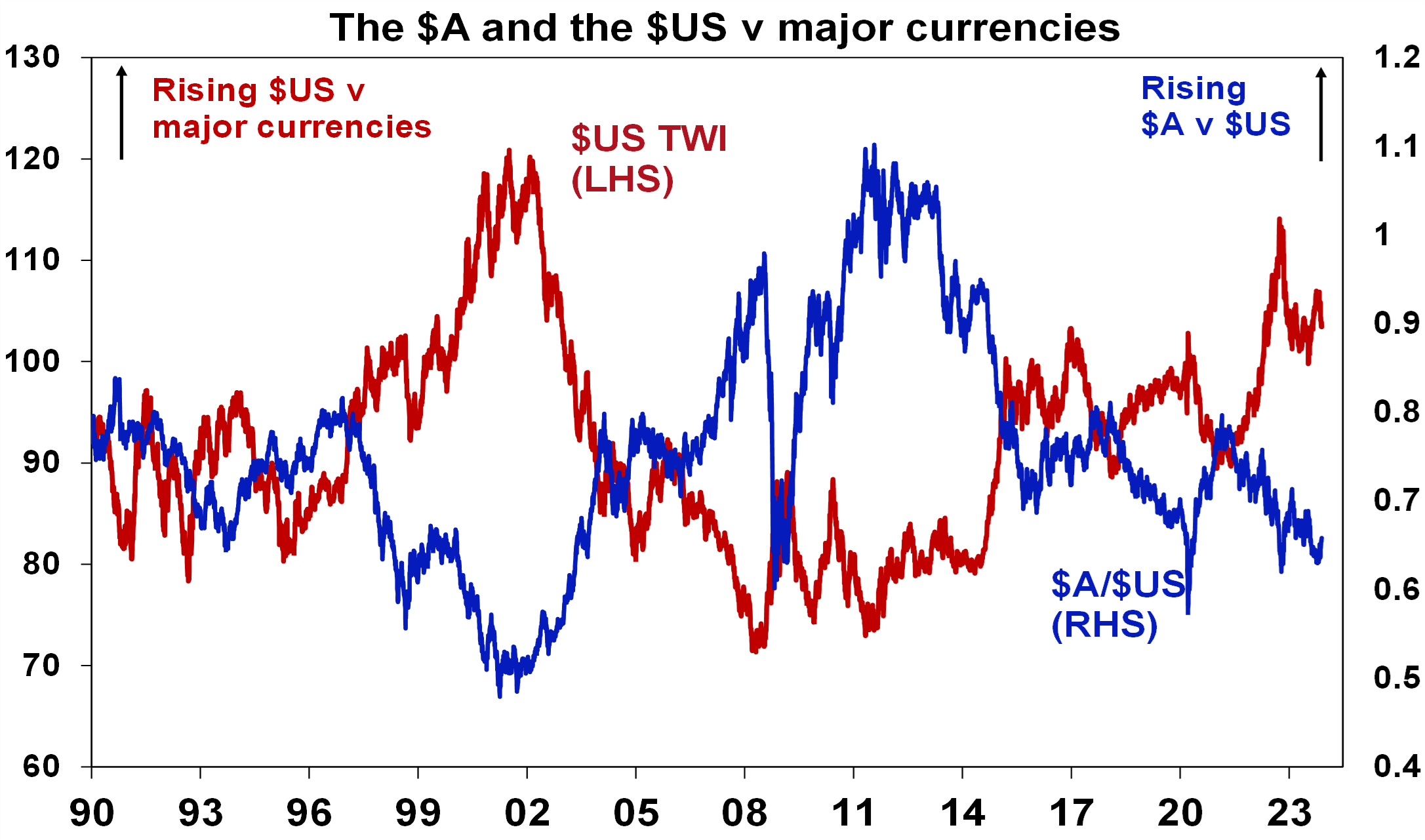

Since reaching $US0.80 in February 2021 the $A has fallen leaving it below its average levels of the last few decades.

Source: Bloomberg, AMP

The downtrend since February 2021 reflects a combination of:

- The initial slow reopening of the Australian economy from the pandemic relative to the US and Europe.

- Worries about a hit to global growth from the inflation surge and higher interest as the $A tends to be sensitive to global growth given Australia’s high proportion of commodity exports.

- This has been accentuated by worries about China with lockdowns last year, a patchy recovery this year and property sector worries.

- A downtrend in commodity prices after an initial boost mainly to energy prices from the Ukraine war.

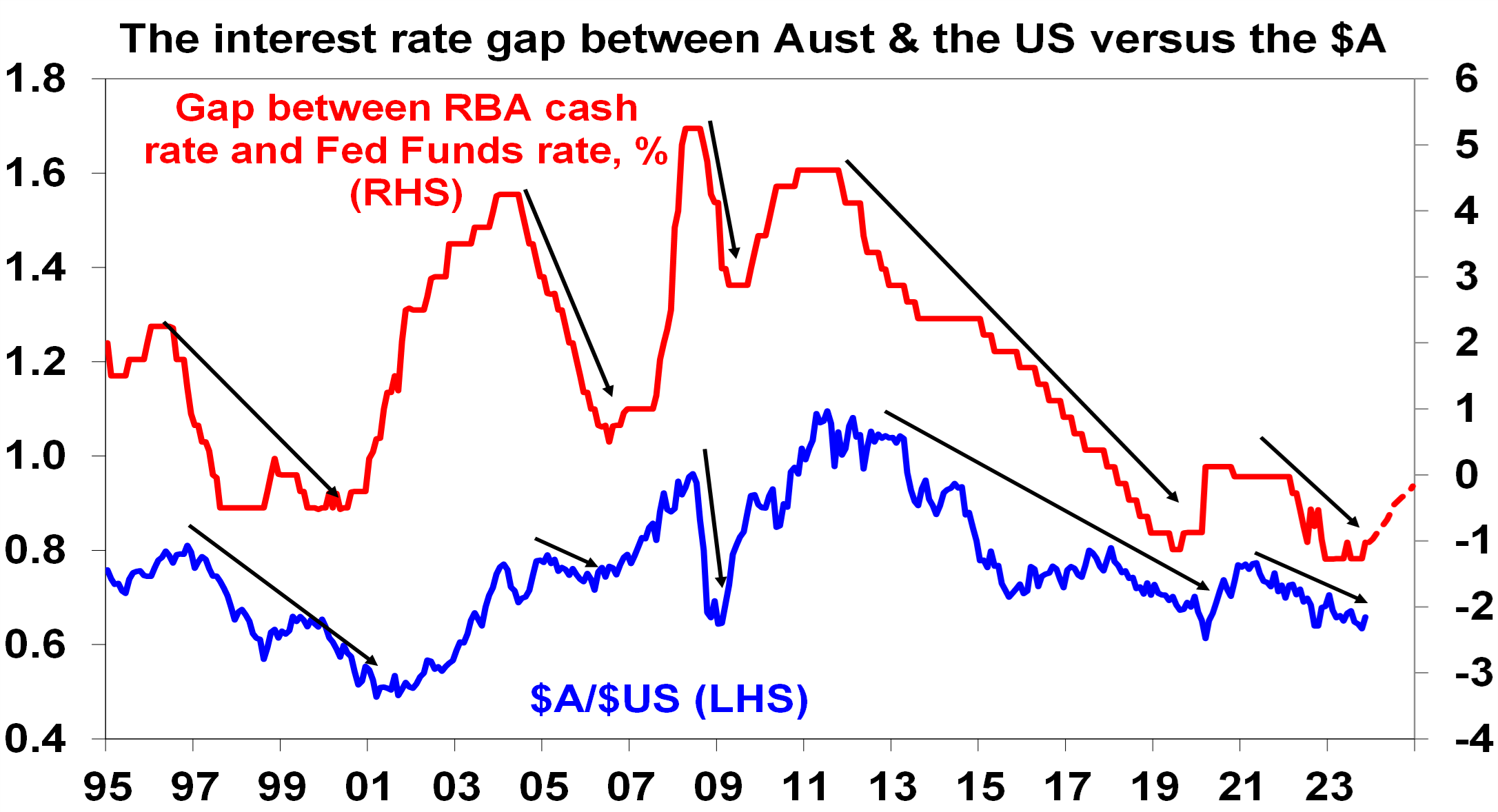

- Less rate hikes from the RBA, compared to the US Federal Reserve which has reduced the incentive for investors to park their cash in Australia. As evident in the next chart the $A tends to fall when the gap between the RBA’s cash rate and the Fed Funds rate narrows (highlighted with arrows) as over the last two years and vice versa.

The dashed part of the rate gap line reflects money mkt expectations. Source: Bloomberg, AMP

- Relative strength in the $US generally (see the first chart above) as it tends to benefit in times of global uncertainty.

But there are five reasons to expect the $A to rise

After hitting a low of around $US0.63 in October the $A has risen to nearly $US0.66 and there’s good reason to expect a further rise.

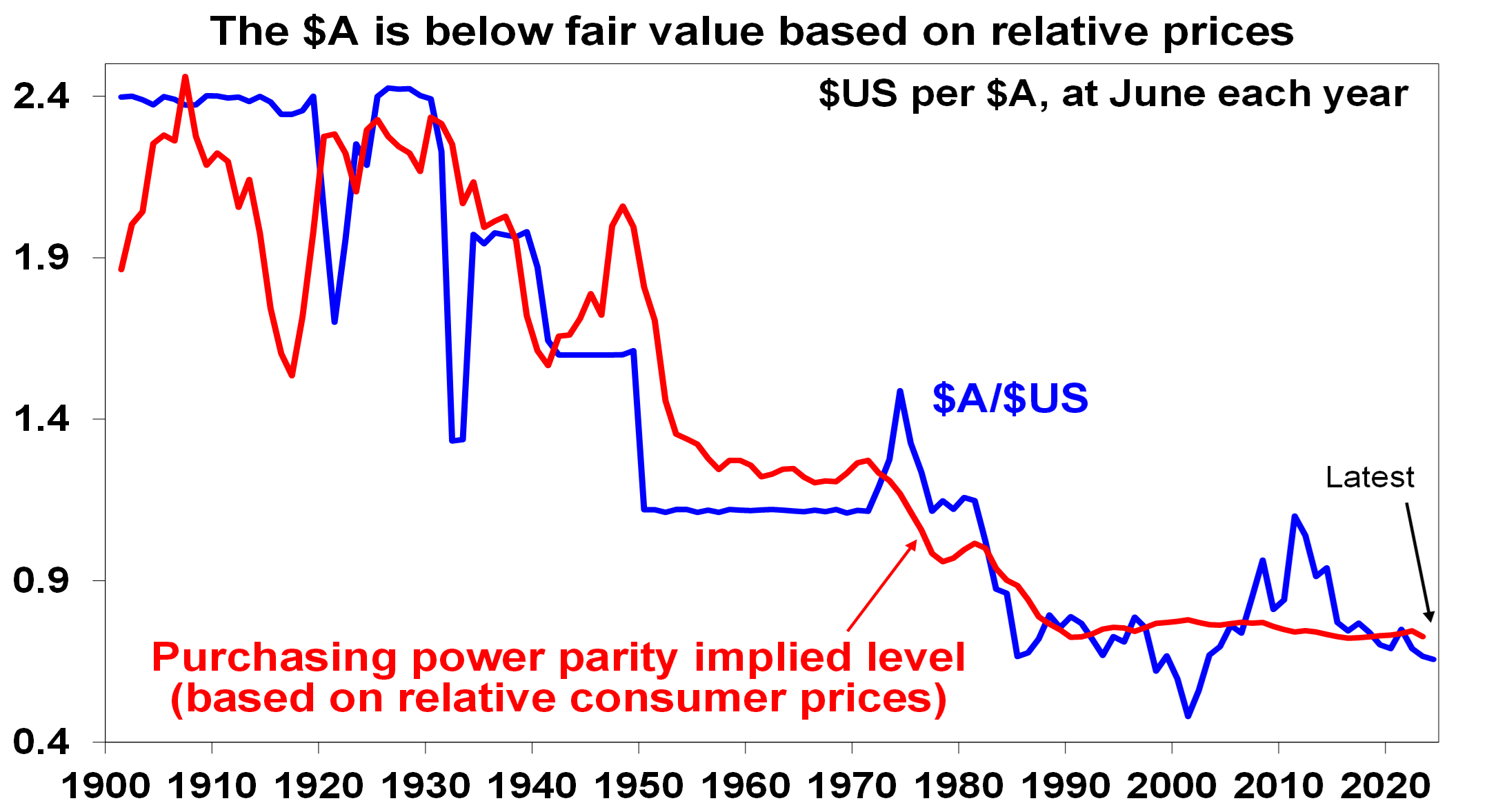

- Firstly, from a long-term perspective the $A is somewhat cheap. The best guide to this is what is called purchasing power parity (PPP) according to which exchange rates should equilibrate the price of a basket of goods and services across countries – see the next chart.

Source: RBA, ABS, AMP

If over time Australian prices and costs rise relative to the US, then the value of the $A should fall to maintain its real purchasing power. And vice versa if Australian inflation falls relative to the US. Consistent with this the $A tends to move in line with relative price differentials – or its purchasing power parity implied level – over the long-term. Over the last 25 years it has swung from being very cheap (with Australia being seen as an old economy in the tech boom) to being very expensive into the early 2010s with the commodity boom. Right now, it’s back to being modestly cheap again.

- Second, relative interest rates are starting to swing in Australia’s favour with increasing signs that the Fed is at the top whereas there is still a high risk that the RBA will hike rates further. Money market expectations show a narrowing gap between the RBA’s cash rate and the Fed Funds rate – see the relative interest rate chart above. More broadly the $US is expected to fall further as US interest rates top out.

- Third, global sentiment towards the $A is somewhat negative and this is reflected in short or underweight positions. In other words, many of those who want to sell the $A may have already done so and this leaves it vulnerable to a further rally if there is any good news.

Source: Bloomberg, AMP

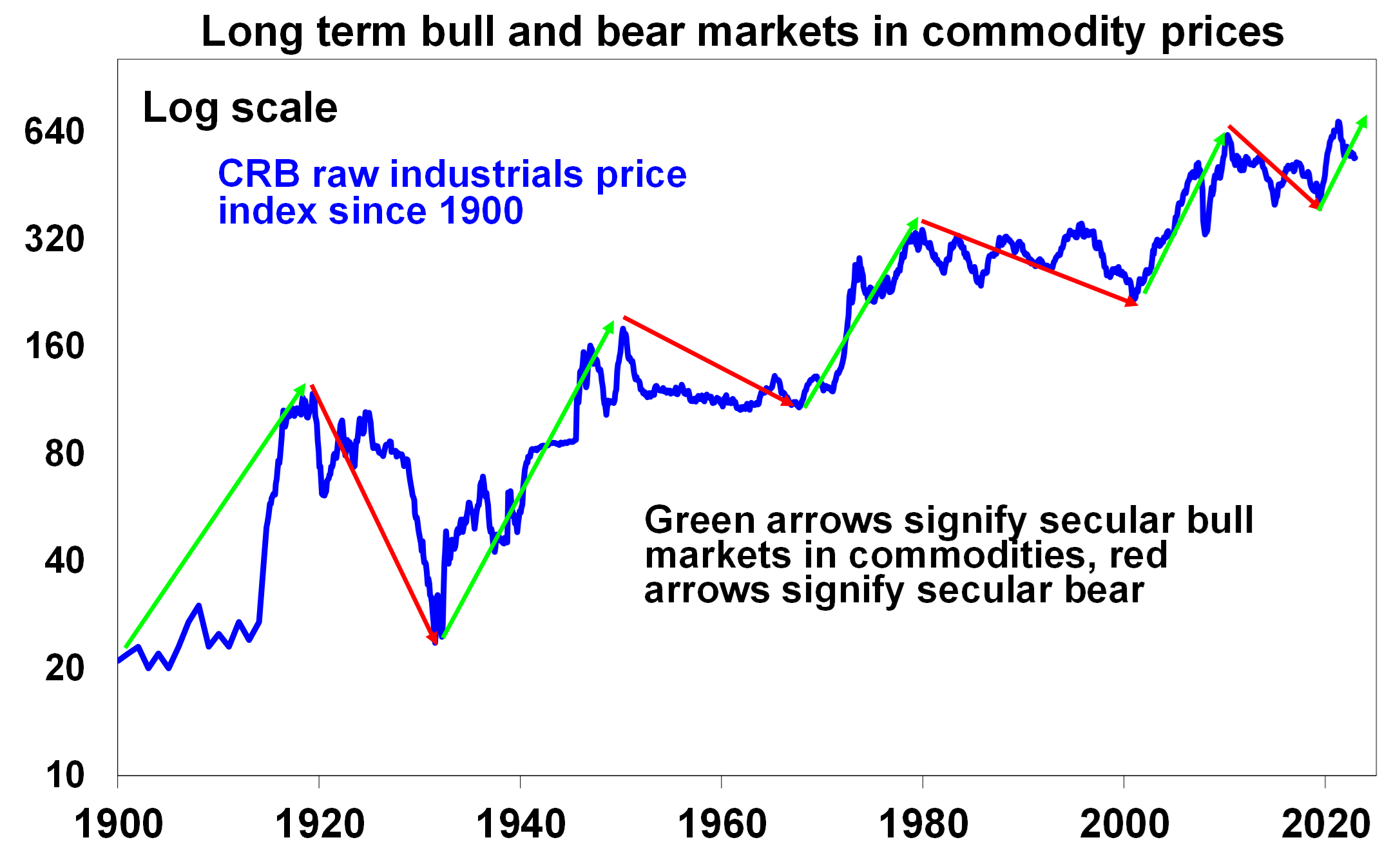

- Fourth, commodity prices look to be embarking on a new super cycle. The key drivers are the trend to onshoring reflecting a desire to avoid a rerun of pandemic supply disruptions and increased nationalism, the demand for clean energy and vehicles and increasing global defence spending all of which require new metal intensive investment compounded by global underinvestment in new commodity supply. This is positive for Australia’s industrial commodity exports.

Source: Bloomberg, AMP

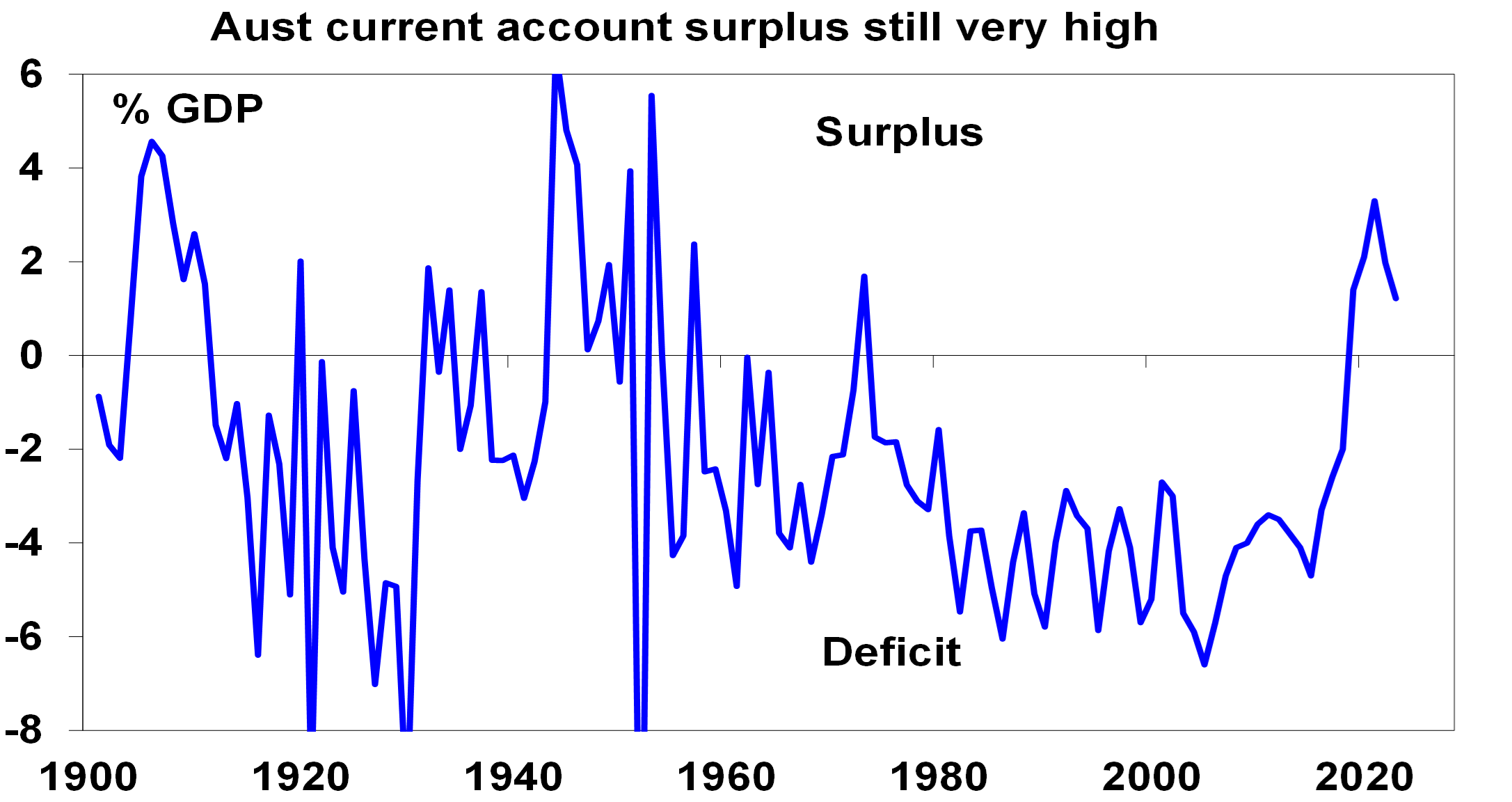

- Finally, reflecting continuing relatively high energy and iron ore prices Australia is continuing to run a current account surplus, albeit its down from recent highs (as gas & coal prices have fallen back and Australians have resumed travelling internationally). The swing into a current account surplus means Australia is a capital exporter and that there is more natural transactional demand for the $A than supply.

Source: ABS, AMP

Where to from here and what is the main risk?

We expect the combination of a slightly more hawkish RBA, a falling $US at a time when the $A is undervalued and positioning towards it still short to push the $A higher into next year, likely taking it back above $US0.70.

The main risk is if the global and/or Australian economies slide into recession next year – this is not our base case but it’s a very high risk and if it occurs it could result in a new leg down in the $A as it is a growth sensitive currency and a rebound in the relatively defensive $US.

What would a further rise in the $A mean for investors?

For Australian based investors, a rise in the $A will reduce the value of an international asset (and hence its return), and vice versa for a fall in the $A. The decline in the $A over the last few years has enhanced the returns from global shares in Australian dollar terms. So, when investing in international assets, an Australian investor has the choice of being hedged (which removes this currency impact) or unhedged (which leaves the investor exposed to $A changes). Given our expectation for the $A to rise further into next year there is a case for investors to tilt towards a more hedged exposure of their international investments.

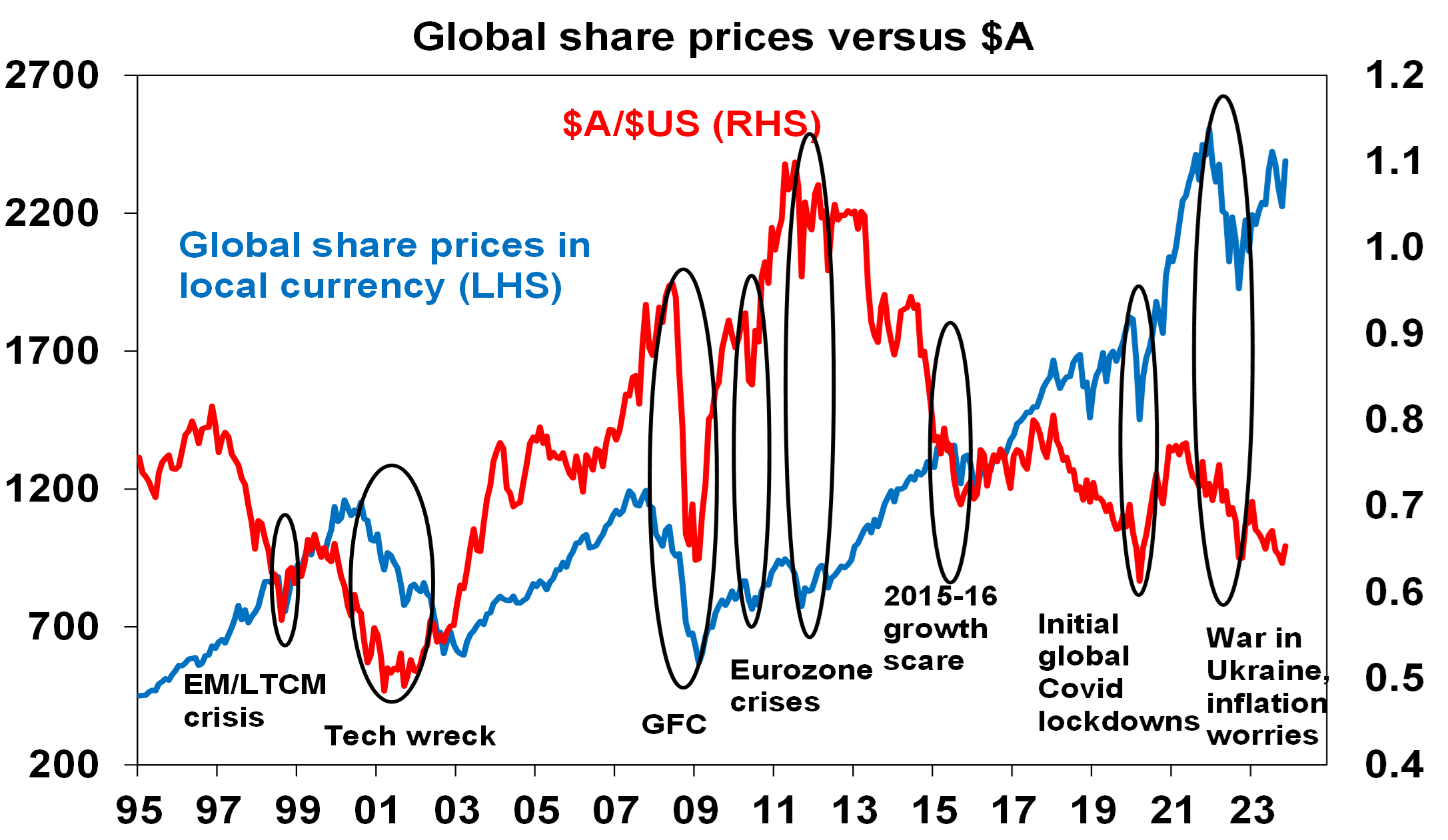

However, this should not be taken to an extreme for two key reasons. First, currency forecasting is hard to get right. And with recession risk remaining high the rebound in the $A could turn out to be short lived. Second, having foreign currency in an investor’s portfolio via unhedged foreign investments is a good diversifier if the economic and commodity outlook turns sour. As can be seen in the next chart there is a rough positive correlation between changes in global shares in their local currency terms and the $A. Major falls in global shares which are circled in the next chart saw sharp falls in the $A which offset the fall in global shares for Australian investors. So having an exposure to foreign exchange provides good protection against threats to the global outlook.

Source: Bloomberg, AMP

What you need to know

While every care has been taken in the preparation of this article, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent AMP. This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.