Key points

– The Australian housing market remains far more complicated than optimists and doomsters portray it to be.

– Australian housing is expensive and highly indebted; but it’s very diverse; mortgage arrears remain low; interest rates still matter; but it’s been chronically undersupplied for years; forecasting home prices is very hard; and housing has similar long-term investment returns to shares.

– The surge in immigration is estimated to push the housing shortfall to around 200,000 dwellings this financial year.

– Price gains are expected to be around 5% this year with high rates dragging but the supply shortfall supporting prices. The risks are finely balanced.

Introduction

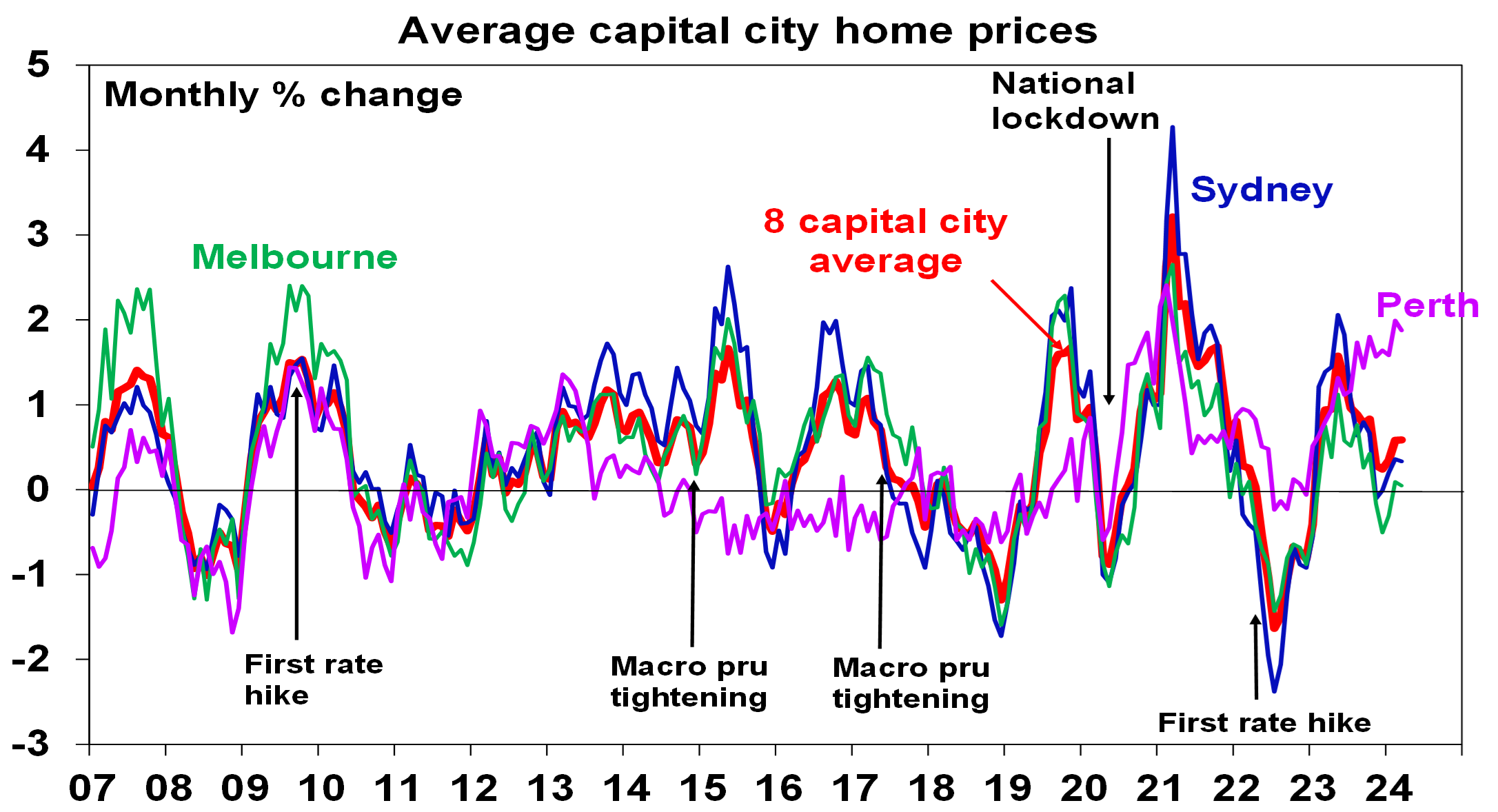

The Australian housing market has started the year on a solid note with national home prices up 1.6% over the first three months according to CoreLogic. We had thought the drag of high mortgage rates would get the upper hand again but the supply shortfall is continuing to dominate.

Source: CoreLogic, AMP

Extreme property views

While most economists sit in the middle, there are basically two extreme views amongst “property experts”. Some real estate spruikers still wheel out the old “property will double every seven years” line. But property doomsters say it’s hugely overvalued and overindebted and so a crash is inevitable. The trouble with the former is that it implies the already high ratio of home prices to incomes will double over the next 12 years! The trouble with the doomsters is that they’ve been saying that for decades. The reality is that it’s far more complicated than the extremes portray it. Here’s seven stylised “facts” regarding Australian property.

First – it’s very expensive

This has been the case since the early 2000s but it’s been getting worse:

- House price to income ratios have doubled since the year 2000.

Source: ABS, CoreLogic, AMP

- The years taken to save a 20% deposit for an average full time wage earner have doubled from 5 years 30 years ago to 10 years now.

- A measure of house price valuation based on the ratio of home prices to rents (a bit like a PE for shares) adjusted for inflation shows house prices around 36% above their long-term average price to rent ratio.

- It’s also expensive in global comparisons, eg, the 2023 Demographia Housing Affordability Survey shows the median multiple of house prices to income at 8.2 times versus around 5 in the US and UK.

The expensive nature of Australian property and the high level of household debt that goes with it leaves the economy vulnerable should high interest rates or unemployment make it harder to service loans and is leading to rising wealth (and intergenerational) inequality.

Second – it’s also very diverse

While it’s common to refer to “the Australian property market”, in reality there is significant divergence between localities. This has been been seen recently with rapid relative price growth in Adelaide, Brisbane and Perth. See the first chart for Perth. This divergence partly reflects a combination of better housing affordability (with prices in Adelaide, Brisbane and Perth playing catchup after lagging pre-pandemic) and relative population growth (with Brisbane and Perth benefitting from interstate migration).

The divergence is reflected in measures of valuation. For example, the next table shows the percentage difference between price to annual rent ratios adjusted for inflation relative to their average since 1983. On this basis while houses are 36% overvalued, units are only 9% over valued. And Perth stands out as the least overvalued market in terms of houses and is actually undervalued (by 12%) in terms of units.

% overvaluation relative to long term price to rent ratios

| City | Houses | Units |

| Sydney | 47 | 12 |

| Melbourne | 24 | 6 |

| Brisbane | 45 | 15 |

| Adelaide | 33 | 24 |

| Perth | 8 | -12 |

| Hobart | 42 | 31 |

| Canberra | 44 | 20 |

| Capital city average | 36 | 9 |

Source: REIA, AMP

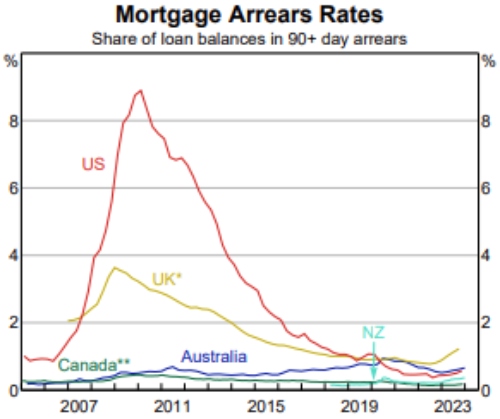

Third – mortgage arrears remain low (for now at least)

Headlines of excessive mortgage stress have been common for over a decade now. There is no denying housing affordability is poor, household debt is high and some households are suffering significant mortgage stress with the two or three fold increase in mortgage rates. But despite this mortgage arrears rates remain remarkably low as indicated in this chart from the RBA’s Financial Stability Review published last month.

Source: RBA Financial Stability Review, March 2024

The low level of arrears partly reflects strong lending standards in Australia combined with the strong jobs market and a high level of savings buffers coming out of the pandemic. That said, arrears are starting to pick up and the risks will rise as buffers run down, scope to cut discretionary spending is exhausted and if the labour market deteriorates significantly.

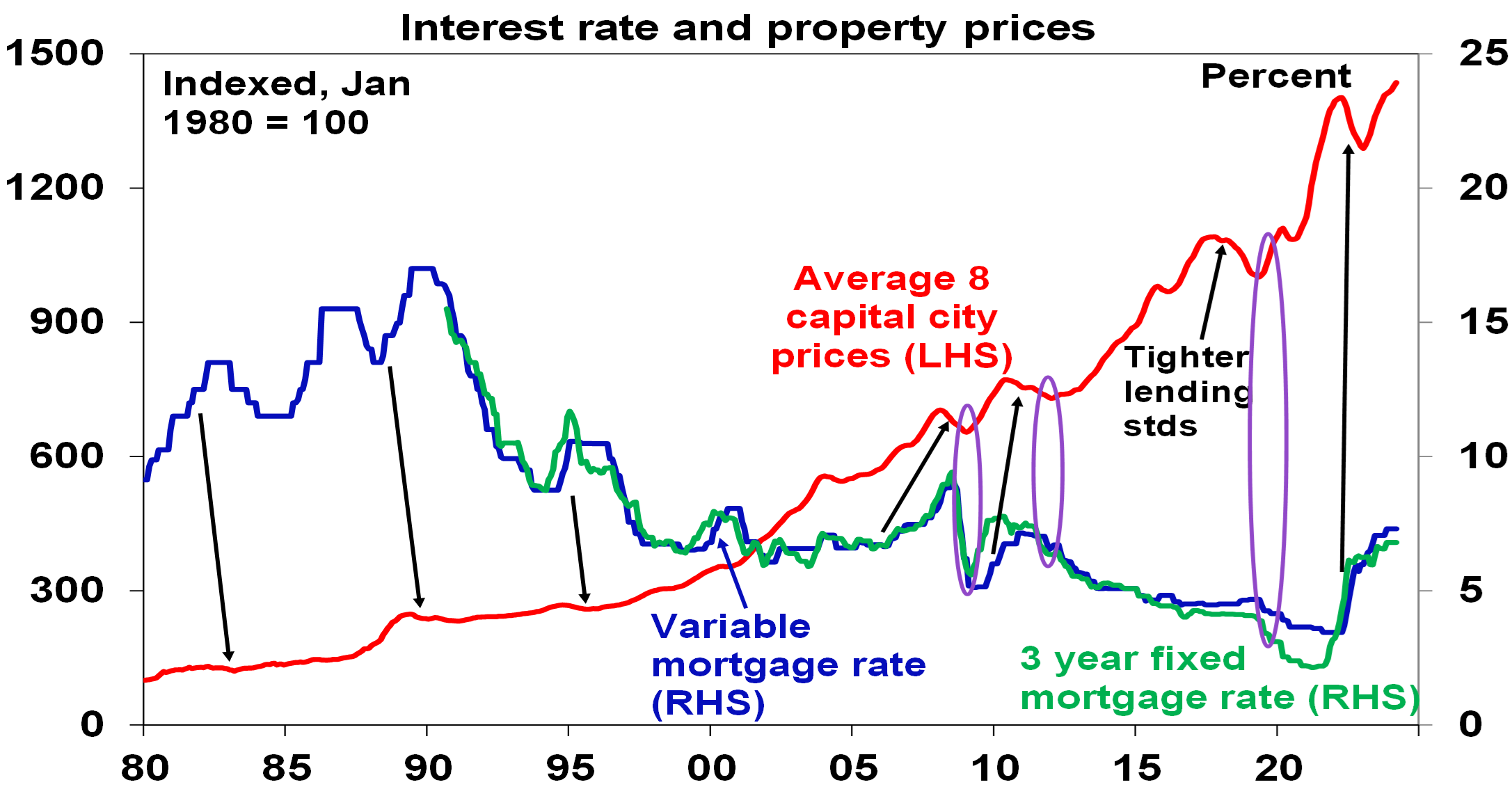

Fourth – interest rates still matter

The long sweep of history shows interest rates matter a lot to the property market. The downtrend in mortgage rates since the late 1980s underpinned the surge in property prices over the same period as it enabled buyers to borrow more relative to their incomes. And rate hikes have been associated with cyclical price falls (black arrows in the next chart) with rate cuts usually needed for upswings (see the purple ovals).

Source: CoreLogic, RBA, AMP

But of course, the impact of interest rates can be swamped by other factors at times, as has been the case over the last year.

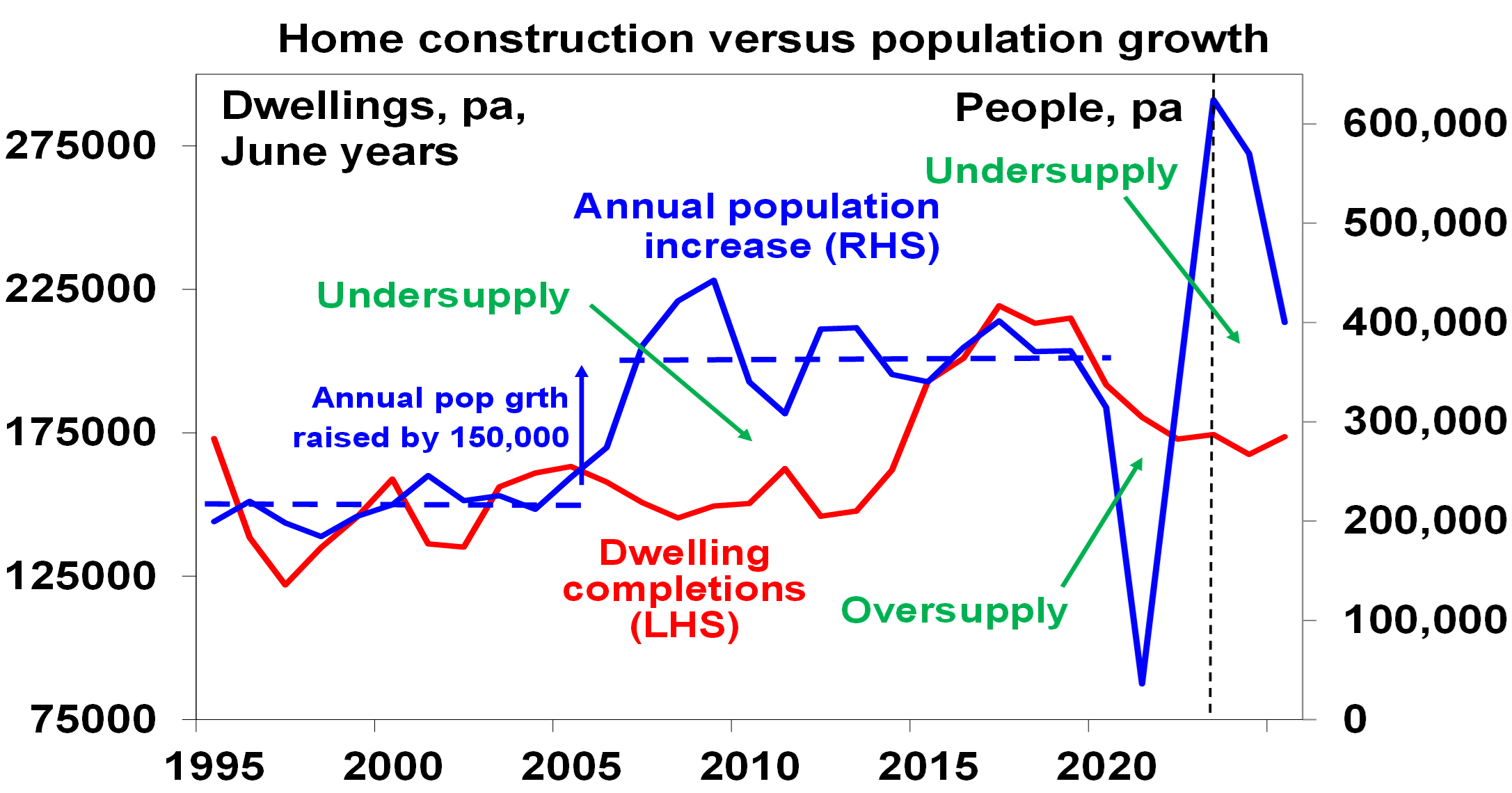

Fifth – it’s chronically undersupplied

This has been the case since the mid-2000s when immigration levels, and hence population growth, surged and the supply of new homes did not keep up. The pandemic’s freeze on immigration provided a brief relief but this was offset by a fall in the number of people per household and the problem has worsened with reopening leading to record immigration levels (of 548,800 people over the year to September resulting in population growth of nearly 660,000). This has pushed underlying housing demand to around 250,000 dwellings pa at a time when home completions are around 170,000 dwellings a year. So, the shortfall of homes is getting worse (and likely to reach 200,000 dwellings by June) and this explains the surprising strength in home prices over the last year. The next chart assumes some slowing in immigration levels, but data up to January suggests it remains around record levels. Given home building capacity constraints and the desire to reduce the existing housing shortfall, immigration levels really need to be cut back to around 200,000 a year.

Source: ABS, AMP

Sixth – forecasting swings in home prices is hard

Failed property crash calls have been a dime a dozen over the last two decades and forecasting property swings has been hard. For example, RBA Governor Michele Bullock noted last month that “I wouldn’t like to predict housing prices…every time we tried…we seem to get it wrong…” So be humble and sceptical when it comes to house prices forecasts.

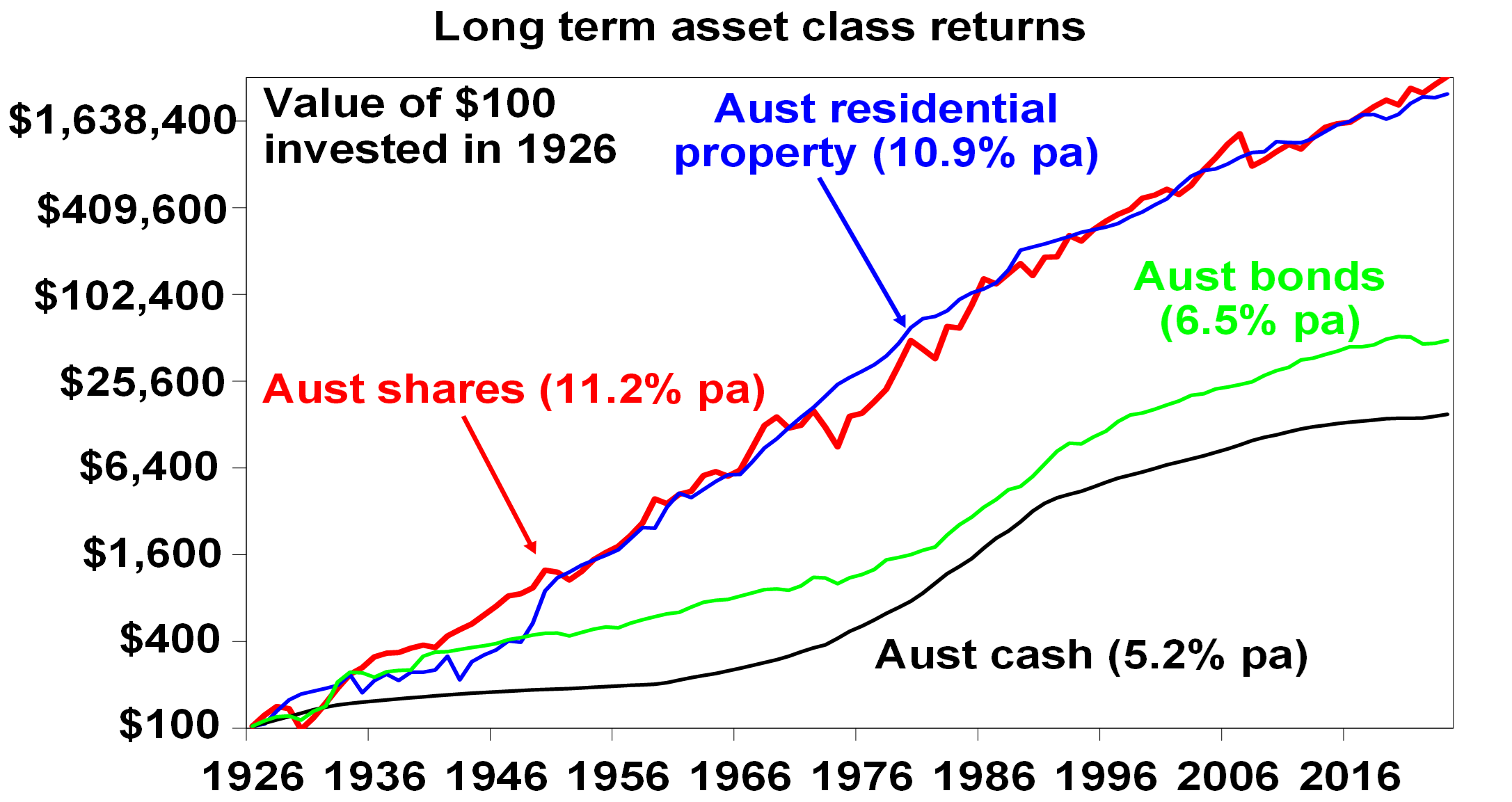

Finally – it has similar long term returns to shares

This can be seen in the next chart which shows the value of $100 invested in 1926 in Australian cash, bonds, shares and residential property with interest, dividends and rent (after costs) reinvested along the way. Over the period both shares and property return around 11% pa. Property’s low correlation with shares, lower volatility but lower liquidity makes it a good portfolio diversifier. So, there is clearly a role for it in investors’ portfolios.

Source: ASX, ABS, REIA, AMP

Where to now?

As we noted earlier forecasting property prices is fraught. Particularly now with the opposing forces of a major chronic supply shortfall and high mortgage rates. Our base case is now for 5% or so home price growth this year, down from 8% last year, as still high interest rates constrain demand and along with higher unemployment lead to some increase in distressed listings. However, the supply shortfall should provide support and rate cuts are expected to boost price growth later this year. Delays to rate cuts and a sharp rise in unemployment would signal downside risks whereas the supply shortfall points to upside risk. The key for savvy investors, given the pressure from high interest rates relative to still low rental yields making most property investments cash flow negative, is to look for properties offering decent rental yields.

What you need to know

While every care has been taken in the preparation of this article, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent AMP. This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.